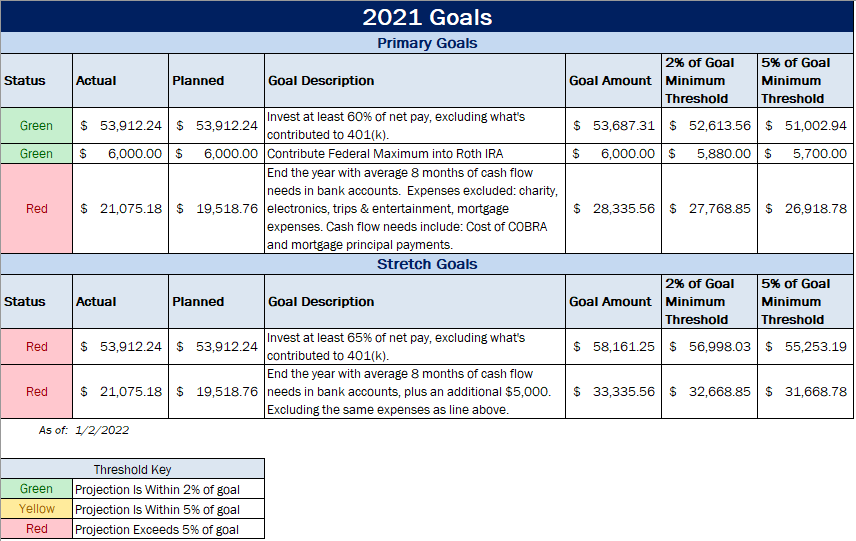

2021 ended with 2 goals met and 1 goal missed. I met targets for investing at least 60% of net pay and maximizing the Roth IRA contributions. I missed the cash in the bank target of $28,000, having only about $21,000.

The bank account goal was missed due to significant cash flows going to unplanned expenses. Even when the goals was set out in early 2021, having $28,000 in the bank was already at risk. Along the year, a few expenses went beyond their planned amount by a total of about $7,000: car maintenance, trips / entertainment, and pet expenses. These, along with few expenses that went under budget and not enough income to offset the increase contributed to a wider than expected reduction in bank accounts.

Head over to the 2021 goals page to get details on each of the goals.

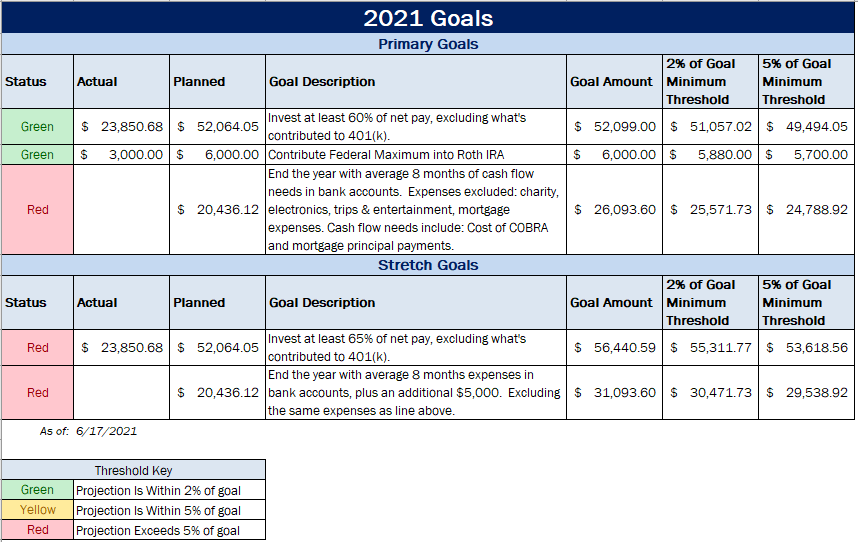

I’m a little late getting my goals posted. I’ve had them formed since Q1 2021 but I’ve been tweaking them since and I am finally ready to settle on my commitments for the year.

Primary Goals

Invest at least 60% of net pay, excluding what’s contributed to 401(k)

Increased from 55% in 2020 to:

Make up for a reduction in 401(k) employer match that was 6% of my contribution

Keep me focused on investing more each year

Represents any investments I make that are not toward my 401(k) because technically net pay already assumes 401(k) is contributed

Contribute Federal Maximum into Roth IRA

Ensures I’m keeping up with the maximum Roth IRA Contributions that I can make under Federal law

End the year with average 8 months of cash flow needs in bank accounts

Provides expected cash needs in case of a an emergency, such as a sudden job loss

Tries to represent a true cash flow need (which includes or excludes certain accounts)

This is projected to not be met due to a relatively high cash burn expected through the remainder of 2021. See below for an explanation.

Stretch Goals

Invest at least 65% of net pay, excluding what’s contributed to 401(k)

An even bigger stretch than the equivalent primary goal

End the year with average 8 months of cash flow needs in bank accounts, plus an additional $5,000

Tries to ensure excess capital is saved (unless invested) as opposed to spent

Why the “average 8 months of cash flow needs in bank accounts” goal is at risk

Trips / Entertainment expenses are looking to be $5,000 more than planned due to a major trip taken in June

I accidentally made a pre-payment towards the mortgage of $450 instead of contributing it toward the payment due.

What I’m doing to correct the issue

Food expenses was approximately 2 times higher than plan so far this year. This was primarily due to eating out more vs. eating at home. I plan to make more food at home to keep this within budget.

Trips / Entertainment in June was unplanned in the budget and as a result was the primary contributor to putting my cash position at risk. I don’t expect to do this again, and future Trips / Entertainment expenses will be carefully scrutinized to hopefully reduce future projected expenses.

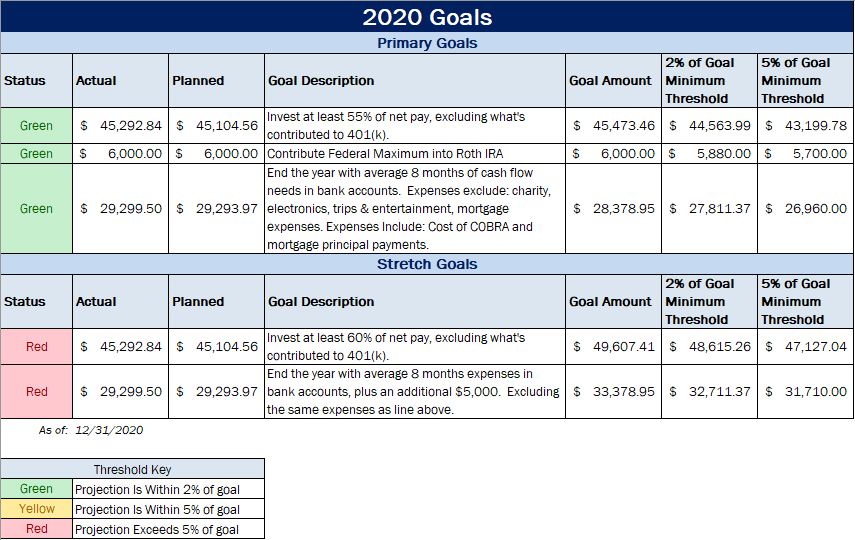

I finished 2020 completing all primary goals as planned, while completing none of my stretch goals. Below is a breakdown of how I ended the year. I expect 2021 goals to be very similar, since I feel these are good targets.